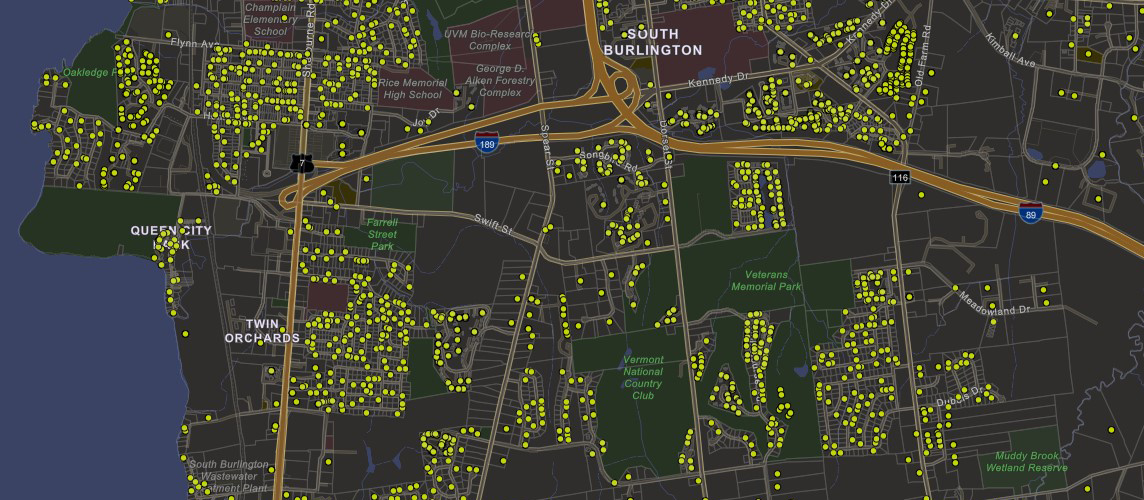

Location data of property transfers (PTTR's) are now available in the Vermont Open Geodata Portal. The dataset provides approximate point locations and associated public information collected by the Department of Taxes under 32 V.S.A. § 9606 for all property transferred by deed in Vermont beginning in January 2019 through present. The layer will be updated weekly. Most transfers (70%) will appear in the dataset within four to five weeks of the sale’s closing date. The property transfer dataset can be used as a supplement to parcel data served by the parcel program which provides an annual snapshot of property ownership as of April 1st and is updated each spring based on the latest statewide Grand List.

Data Access

The data will also be available to view within the Parcel Viewer later in 2024. They are also linked from the parcel page at the Vermont Open Geodata Portal.

Content and Mapping

The layer contains PTT-172 and PTT-175 data as received from the Department of Taxes, with five additional fields: latitude, longitude, standardized town name (based on town code), town GEOID, and the match method used for geocoding. Transfers that could not be geocoded because of an incomplete or invalid SPAN or property address are still retained in the data table but are not represented spatially and do not include coordinates.

More details about the data and methodology can be found at the Property Transfer Tax webpage.

Multiple methods were used for geocoding property locations; in order of priority and precision these are:

- Geocoded using the VCGI ESITE Geocoder with the property street and city. MatchMethod = Property Address (ESITE). If unmatched:

- Match on SPAN in the E911 Site Locations layer; geocode using the location of the ESITE. MatchMethod = SPAN (ESITE). If unmatched:

- Geocode using the VCGI Composite Geocoder with the property street and city. MatchMethod = Property Address (Composite). If unmatched:

- Match on the SPAN in the Standardized Parcel Data layer; geocode based on a point located within the parcel polygon. While the point will fall within the correct parcel it may still be distant from the actual property, particularly in large parcels, and is the least precise. MatchMethod = SPAN (Parcel centroid).

- Properties that cannot be geocoded using the methods above are listed as Unmatched.

Questions?

For questions specific to property locations as shown in this GIS layer, please contact VCGI at vcgi@vermont.gov.

In addition to details about ownership, the data layer contains several date fields that allow one to view property transfers not just by location but also by time. For example, this animation shows transfers that closed in central Vermont through 2019, 2020, 2021, 2022, and then 2023.

Frequently Asked Questions

Click on a frequently asked question below to see an answer. FAQ answers are subject to change.

In Vermont, town and city clerks are responsible for maintaining and updating land records. This includes receiving, recording, and indexing all land-related documents filed with the town or city. Any new deeds transferring ownership are typically provided to the town or city clerk by the seller’s attorney (closing date). Once filed, the clerk submits the information to the Vermont Department of Taxes (received date). The transfer record is then reviewed and posted (posted date). Finally, VCGI processes newly posted property transfers each week to update the map. As of December 2023, we see the following distribution between closing and posted dates:

- 1% in less than one week

- 30% within one week

- 21% in one to two weeks

- 11% in two to three weeks

- 7% in three to four weeks

- 30% in over four weeks.

- Of these, 17% are over two months, 8.5% are over six months, and 5% are over one year.

Including the weekly update cycle of the map, viewers can expect the map to show 70% of transfers within four to five weeks of the property’s closing date.

There are a few reasons why a transfer that has occurred does not appear on the map. One is the delay between a closing, receipt of the new ownership information by the town or city clerk, filing and documentation of the transfer by the clerk, submittal of the transfer to the Tax Department, review and posting of the transfer, and publishing the transfer record to the map. Approximately 60-70% of transfers will appear on the map within a month of the closing date, with 30% appearing within one to two weeks. In other cases, records may not appear for a month or longer due to the multiple steps of the submittal and review process.

Another explanation for a property transfer missing from the map is incomplete or invalid attribute information used to determine the property location. Several methods are used to determine the physical location of the property address (geocoding) when VCGI receives records from the Tax Department. These methods rely on the property address or the property SPAN. In some cases, neither of these data fields contain sufficient valid information to geocode the property. Properties falling into this category will be shown in the data table but will not have coordinates or a point location on the map. These properties are listed as “Unmatched” in the Match Method field and currently account for approximately 4.5% of records. The majority are timeshares. Users should check the data table in addition to the map to see if a property transfer has been captured.

All point locations are approximate but may vary in their level of precision. The geocoding process utilizes several methods to locate properties, indicated for each transfer in the MatchMethod field. In order of priority, these methods are:

- Geocoded using the VCGI ESITE Geocoder with the property street and city. MatchMethod = Property Address (ESITE). If unmatched:

- Match on SPAN in the E911 Site Locations layer; geocode using the location of the ESITE. MatchMethod = SPAN (ESITE). If unmatched:

- Geocode using the VCGI Composite Geocoder with the property street and city. MatchMethod = Property Address (Composite). If unmatched:

- Match on the SPAN in the Standardized Parcel Data layer; geocode based on a point located within the parcel polygon. MatchMethod = SPAN (Parcel centroid).

- Properties that cannot be geocoded using the methods above are listed as Unmatched.

The first two methods provide the most precise location. The Composite geocoder uses a combination of E911 ESITEs, road names, and address ranges. In the absence of an exact address match, the Composite will interpolate between known addresses along a road to assign the location. Consequently, the point may fall near to but not precisely at an actual property location. The SPAN (Parcel centroid) method is the least precise and simply creates a point somewhere within the parcel matching the SPAN. For large parcels in particular the location may be distant from any physical property located on that parcel. Verifying the MatchMethod used to geocode a property can help inform why offsets may exist.

VCGI geocodes property transfers to report the coordinates, standardized town name, town GEOID, and Match Method. Beyond that, property transfer data are published exactly as received from the Tax Department as reported by taxpayers. Inquiries about any errors or issues should be directed toward the Tax Department at tax.rett@vermont.gov. In rare instances returns need to be amended; once processed, they will replace the existing return in the dataset.

The display of property and ownership information operates on three different time scales:

- Property transfers happen the fastest. The time between a closing date and seeing the data on the map can be as short as one or two weeks. Transfers happen daily, returns are processed continuously, and the dataset is refreshed weekly for all of Vermont.

- Parcel geometry changes (subdivisions, boundary line adjustments, etc.) also happen continuously, but are performed by municipalities and reflected less frequently. Most municipalities, or their mapping vendors, submit parcel geometry to VCGI annually. VCGI typically reviews and publishes updated parcel geometry within one to three weeks of receipt. Like property transfers, parcel geometry is refreshed weekly for any municipalities that have submitted new data. The status of each municipality’s parcel data can be found in the Town Mapping Status viewer. For additional detail on parcels, see the Parcel Program.

- The statewide Grand List is published annually on April 1 for the previous year. The Grand List is updated by the Tax Department and compiles property ownership information as submitted by each municipality. The tabular data from the Grand List is linked to parcel geometry using the SPAN, which is a unique parcel identifier. VCGI typically joins the most current parcel data to the latest version of the Grand List by early May each year.

Since the Grand List is updated once per year, it does not reflect real-time property ownership. Any transfers that occur after April 1 will not be included in the annual Grand List for over a year (e.g., the 2021 Grand List is published on April 1, 2022. Updated ownership information from a sale in May 2022 will not appear in the Grand List until the 2023 edition, released April 1, 2024). The property transfer dataset provides an intermediate update on ownership information that may not yet exist in the latest version of the statewide Grand List. While the property transfer dataset currently only contains records dating back to 2019, it can also be a simple and fast method for viewing ownership changes over time.

Users will be able to see each time a property was transferred between January 2019 and present (note: 70% of transfers will appear on the map within four to five weeks of the closing date, but this can be shorter or longer). Transfers occurring before 2019 are not currently included in the dataset.

Included in this dataset are relevant lines items from the Property Transfer Tax Returns, the PTT-172, and PTT-175. This dataset is reported by the taxpayers and accepted by the Tax Department. The Department presents data as-is. The data are posted in weekly and monthly formats; VCGI processes new records weekly.

A property transfer tax is a one-time tax on the transfer by deed of title to real property in Vermont.

Vermont’s land gains tax is a tax on the sale or exchange of subdivided land in Vermont which is held for less than six years.

The property transfer tax is paid by the buyer (transferee) of the property.

A primary residence is a property that is used as a principal residence within one year of the transfer or two years if the buyer will build and occupy as their principal residence on transfer of land only. A secondary residence is a place that is occupied part-time or less than the majority of the calendar year.

A special rate of 0.5% tax is available for up to $100,000 of the value paid or transferred for a property that qualifies as a principal residence. In addition, a principal residence that qualifies for Exemption 99 will have no tax due on the first $110,000 of the value paid or transferred and a reduced 1.25% tax for values of more than $110,000 and less than $200,000.

The general property transfer tax rate is currently 1.45%, including a 0.2% surcharge for the Clean Water Fund.

The SPAN is an abbreviation for the School Property Account Number. This number is found on the property tax bill. In addition, there is a SPAN Finder available on the tax department’s website.

The total amount due in property transfer tax is shown on the property transfer tax return (Form PTT-172). A property transfer tax return must be filed with a town clerk whenever a deed(s) transferring title to real property, this is delivered to a town clerk for recording. When a transfer is made by deed, the buyer or transferee is liable for the transfer tax. When acquiring a controlling interest in an entity that holds title to property, the person making the acquisition is liable and all persons acting in concert to acquire a controlling interest are individually liable.

In 1978, the Vermont legislature passed a law establishing the use value appraisal of agricultural, forest, conservation, and farm buildings property. Today this program is known as “Current Use” and is administered by the Division of Property Valuation and Review (PVR) within the Vermont Department of Taxes. The property transfer tax return includes entries for whether the property is enrolled in the Current Use Program and whether the enrollment will continue. When a property is transferred, the new owner is required to submit a Current Use application within 30 days of the recording date to remain in the program.

Typically the seller (transferor) of the property provides the self-reported information found on the property transfer tax return (PTT-172).